A Polarizing Q4

/Q4 Is All About November

Comparing this Q4 so far to that of last year, we’ve observed a 17% increase in revenue, a 20% increase in impressions, and a 2% decrease in CPMs. In aggregate, we’re seeing a successful Q4 with some publisher volatility across the board. However, with Thanksgiving falling later than last year, this November will miss out on 6 big revenue days. You may remember that we saw 2018 November’s revenue at 28% over October’s.

Surprising Publisher Impression Fluctuations YoY

We expected more consistency among our publishers when it came to impressions, but that is not the case. Comparing impressions from Q4 to the same time frame last year, we observed:

Many publishers experienced increases in impressions coupled with decreases in CPMs and vice versa.

Only 3 publishers saw both a major spike in CPMs and impressions YoY.

Partners’ (SSP) See Changes in CPMs

Comparing CPMs of partners’, we saw that some small partners’ experienced large increases in CPMs YoY while large and mid-size partners were more varied. We observed:

4 partners, most with no scale, grew 50% in CPMs YoY. The one exception was Oath, which grew 50% plus.

Partners that offered both scale and big CPM increases include:

OpenX CPMs increased by 18% YoY.

Index Exchange CPM’s increased by 27% YoY.

Rubicon CPM’s increased by 21% YoY.

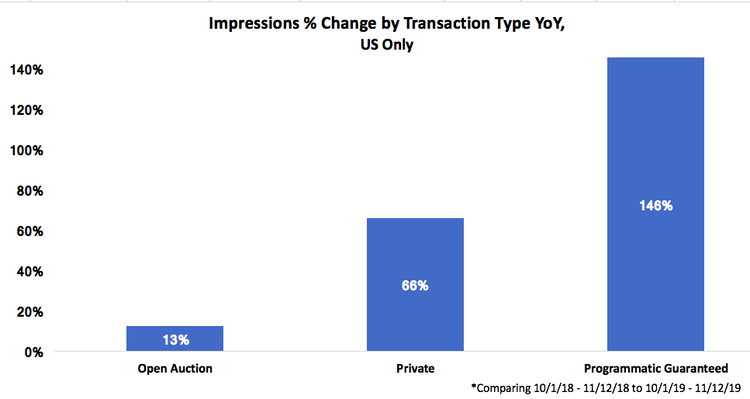

Large Publishers Winning With Private and PG

When comparing impressions by transaction type, we observed a significant increase YoY in private and programmatic guaranteed which has been driven by a handful of large publishers that average over a billion impressions a month.

Open Auction experienced a 13% increase in impressions and flat CPMs.

Private is up 66% but saw CPMs dip by 25%.

Off of a very small 2018 base, Programmatic Guaranteed experienced a 146% growth in impressions and a 13% increase in CPMs.

A Note About the Data this Week

If you follow our emails closely, you’ll note that in our last email when looking at October revenue over prior year we saw only modest growth. We have since increased the size of our benchmarking pool and have excluded two publishers that were anomalies.

In addition, we excluded Amazon from this analysis. This is disappointing as this is the time of year we expect to see Amazon deliver their best revenue and CPMs. However, they have been unable to deliver consistent data in the past few weeks. We are hopeful they resolve this issue soon. Facebook has also been excluded. They do not provide a 12 month look back window, so we are left with the option of removing publishers who have been added in the past six months or removing Facebook :(

Week At A Glance