Top 50 Weekly Advertiser Gainers & Decliners 7.21 Week 29

/Top Gainers and Decliners

Below is a weekly view of the top 50 advertisers, based on spend. The right column compares last week to the average of the last 29 weeks.

Below is a weekly view of the top 50 advertisers, based on spend. The right column compares last week to the average of the last 29 weeks.

Week 28 returns to the positive revenue trends we observed at the end of Q2. While we continue to see increased spending from some of the consistent advertisers, the overall start to Q3 is a bit choppy. Trends should become more clear with next week's data.

It's a small world after all. Disney up 23% and spending at pre-covid levels as the parks reopen. However, they are still down compared to where they were in January & February.

Groupe Renault up 56%, with Ford and Volkswagen also continuing their upward trends that began over the last few weeks.

Lending Tree up another staggering 209% having their (7th) highest week of the year. They have become the 5th largest spender in our dataset.

HP up 154% and Dell up 46% with their highest weeks of the year.

Notable decliners: Microsoft, P&G, Facebook, Bayer, and Pfizer having a slow start to the quarter all with their lowest weeks of the year.

Next Up: Our 1H 2020 Report will be released in the next 2 weeks. Please keep an eye out for our recap analysis.

As we make our way into the 2nd half of the year, we understand the importance of evolving our metrics for this report that will make the data more actionable. We will release further details and, hopefully, a new format next week.

Below is a weekly view of the top 50 advertisers, based on spend. The right column compares last week to the average of the last 28 weeks.

Week 27 crosses Q2 and Q3 and encompasses the (generally outdoors) July 4th holiday. Some advertisers continued to have strong market presence, however overall we observed typical Q3 drops attributed to exiting a quarter into a holiday weekend.

As this week doesn’t paint a full picture, we won’t have a good read on Q3 until next week.

Additionally, we are keeping an eye on how the Facebook ban will impact a shift in paid media to the programmatic market and hope to have more meaningful data on this next week as well.

Notable decliners: Microsoft, T-Mobile, Clorox, and Liberty Mutual following a trend that most advertisers are showing as they enter the new quarter and holiday.

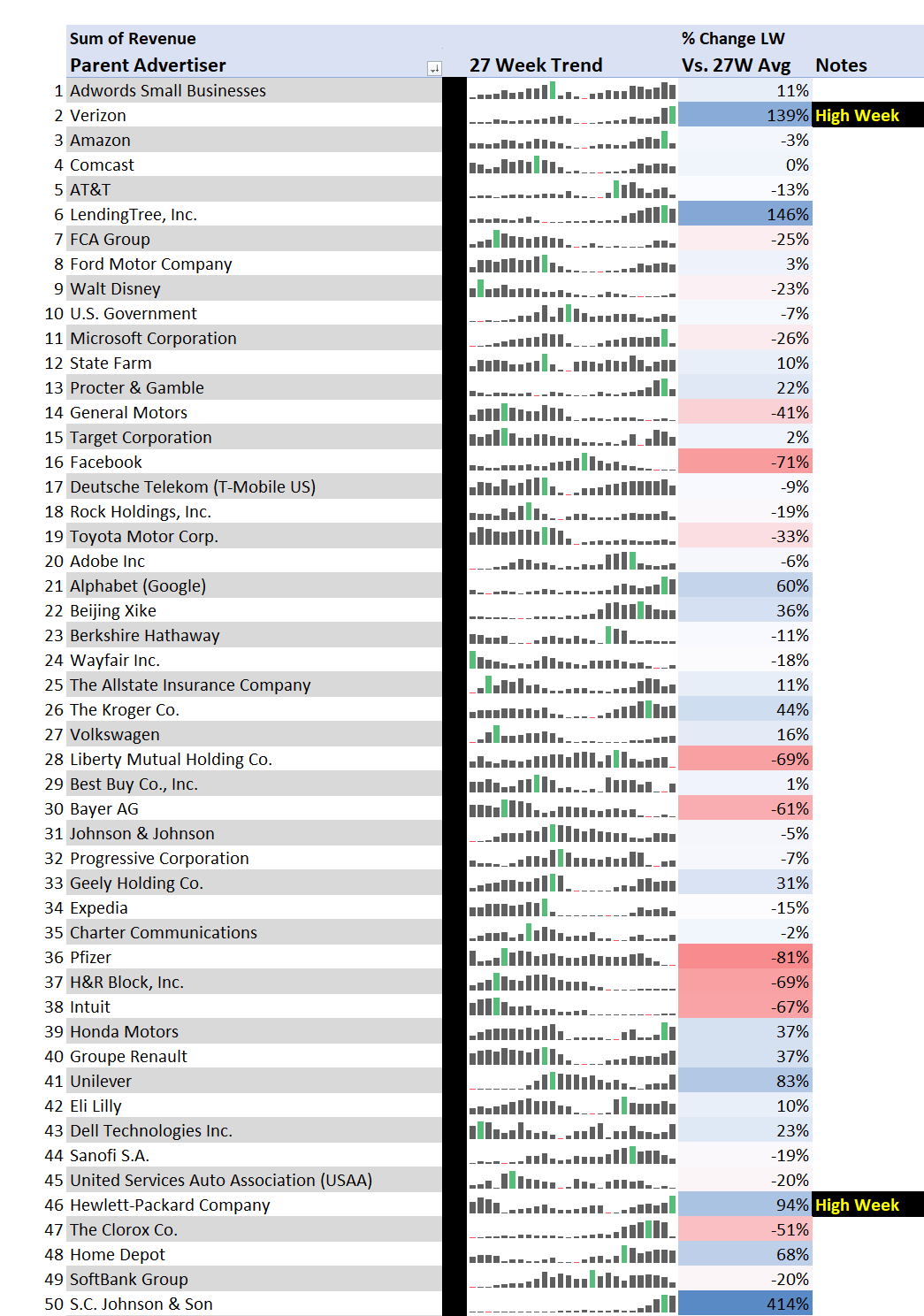

With their relevant product mix, SC Johnson (Saran, OFF!) up a massive 414%, the largest increase this week.

Verizon up 139% and HP up 94%. Both with their highest weeks of the year, and continuing trends of heavy spending relative to the rest of the market.

Not throwing away their shot, Disney saw a large increase with the release of Hamilton. However, they are still down from what they were spending earlier this year.

Lending Tree up 146% continuing its substantial marketing efforts. They are one of the largest advertisers we measure and should be in the top 5 by next week.

THIS FRIDAY: Mondelēz will be joining the next Insights by STAQ presentation July 10 at 1:15pm EST to talk about a Marketer’s Perspective, and The Path Through 2020. Register Here.

Below is a weekly view of the top 50 advertisers, based on spend. The right column compares last week to the average of the last 27 weeks.

Week 26 shows some of the strongest signs of recovery we’ve seen with 10 of the Top 50 advertisers experiencing High Weeks, up from 3 last week. We observed increased growth from consistent advertisers, and the return of absent ones to the market. (And not shown here, CPMs are up as well!)

Whether this is a result of typical seasonal spending, or an opportunity to make up for lost gains remains to be seen. Nevertheless this is welcome news heading into Q3.

Consistently a Top 15 spender, Microsoft up 99% with its highest week of the year.

Honda up 79% with their highest spending week of the year, and showing gains for the first time since early June. 5 Auto advertisers are up this week, and will most likely continue through the Holiday weekend.

Lending Tree jumps into the Top 10, up 244% and having its sixth consecutive highest week.

Diageo who’s been mostly absent from the market, up 596% with its highest week of the year. Pernod Ricard also up this week. Is it the typical July 4th Holiday or are we seeing the ultimate in targeting and they know we collectively need a drink?

Other notable movers: McDonald’s up 174% and Lenovo up a massive 603%, both increasing spend by 10x over the last 4 weeks.

First Look: Mondelēz will be joining the next Insights by STAQ presentation July 10 at 1pm EST to talk about a marketer’s perspective, and the path through 2020. Register Here.

Below is a weekly view of the top 50 advertisers, based on spend. The right column compares last week to the average of the last 26 weeks.

After months of volatility, Week 25 shows the positive upward trends we’ve been waiting for.

While category movement has been the recent story, the return of some bellwether brands is finally driving significant momentum. Whether these spend levels are sustained remains to be seen, but we will take this as good news heading into Q3.

The biggest advertiser we’ve had our eye on to return is finally coming back. FCA is up 11%, and spending for the first time since March. This may be a response to Ford, also up, increasing over the last couple of weeks. Including Volkswagen, 3 Auto advertisers in the Top 50 are up and hopefully they will continue to try to make up for lost ground through the summer.

In a welcome return, McDonald’s up 88% and spending for the first time since pre-Covid. They’ve been a surprisingly absent advertiser given their social distance set up with drive thru and take out. We’ve been awaiting this return as another positive sign for recovery, and expect other QSR’s to follow suit.

Consumer Goods up 163% with their second highest week of the year in a row. This is led by an increased spend of Proctor & Gamble, Clorox, and SC Johnson, all experiencing over 100% gains this week.

Retail Trade up 35% with its highest week since March. These gains are led by Target, Wal-Mart, Kohl’s, and Walgreen’s. After being mostly dormant in 2020, Walgreen’s is up 236% showing real spend for the first time this year.

Below is a weekly view of the top 50 advertisers, based on spend. The right column compares last week to the average of the last 25 weeks.

Below is a weekly view of the top 50 advertisers, based on spend. The right column compares last week to the average of the last 24 weeks, which is the metric we use for analysis unless otherwise noted.

Good news this week, revenue and CPMs are on an upward trajectory again. However, specific advertiser moves are inconsistent and hard to decipher. Some Q2 mainstays, like State Farm and Adobe, are pulling back. Whether they maintain their lower spend levels remains to be seen.

Consistently a Top 5 spender, Amazon up 33% with its highest week of the year.

Lending Tree up 216% having its highest spend for the fourth week in a row. If they continue on this path, they’ll likely break the Top 10 by next week.

Consumer Goods up 103% led by the continued spend of Proctor & Gamble, SC Johnson, and Clorox which is up 184%. They all had their highest weeks of the year.

Retail Trade up 23%. The positive gains are driven by the return of Wal-Mart and Kohls up 284% with its highest spend of the year. As shoppers return, so do the advertisers.

Surprisingly, Allstate is back in the top 50 and up 64% while the rest of the category is down for the first time in 5 weeks.

Webinar THIS THURSDAY June 18 at 10:30am EST: State Of Digital Advertising: Where We Are, And The Path To Q3. Register here.

Below is a weekly view of the top 50 advertisers, based on spend. The right column compares last week to the average of the last 23 weeks, which is the metric we use for analysis unless otherwise noted.

After 3 weeks of steady revenue increases, we have seen the market pull back over the last week. The advertiser shifts are likely due to the protests. It is clear that many advertisers may not know how to respond, don’t have appropriate messaging, or are choosing to avoid the content.

That said, we’ve seen spend return from advertisers who have been absent since March. We anticipate this may prompt a return from the other key spenders in those categories.

Ford up 7% with its largest gains in the last 11 weeks. Mazda rose 22%, increasing for the second week in a row and likely breaking into the Top 50 by next week. Nice to see positive signs from Auto, and hopefully this initiates spend from FCA and the rest of the category.

Expedia up a welcome 37% and gaining for the second week in a row. It will be great if others like Marriott follow their lead. Who’s looking forward to travel (advertisers) again?

Lending Tree up 187% having its highest spend for the third week in a row. Looks like they have found a way to capitalize on the current landscape.

Some consistent spenders declining this week are: Adobe, Target, Wells Fargo, Apple, Capital One, and Unilever who had their lowest week of the year. We expect this is a result of current affairs.

Webinar THIS WEDNESDAY June 10 at 12pm: How Publishers Can Generate Ad Revenue Now! Andy Ellenthal will be joined by speakers from Duration Media, Pubmatic, and Confiant, to discuss actionable ideas that help to drive revenue for publishers. You can register here.

Below is a weekly view of the top 50 advertisers, based on spend. The right column compares last week to the average of the last 22 weeks, which is the metric we use for analysis unless otherwise noted.

We have seen 3 consecutive weeks of revenue increases with several categories moving in an upward direction. We expect the trends to continue, but it is hard to anticipate how the events that transpired this past week will impact advertiser behavior. Regardless, we hope the outcome is positive lasting change.

Mobile & Wireless up 70% led by the continued spend of Verizon, AT&T, and T-Mobile. Verizon was up 47% with their highest spend of the year.

Progressive up 24% continuing the trend of consistent spend we have been seeing in the Insurance category. They are still far from State Farm who just had their highest week of the year.

Lending Tree up 174% having its highest spend for the second week in a row. Looks like they’re on their way to being a top 5 spender.

Honda, gaining over the last 2 weeks, is up 24%. Mazda is up a big 136% but is still ranked 95 in spend. It would be great to see FCA back, notice they are still ranked number 5 with almost no spend in the past 10 weeks.

In a surprise return for Travel, Expedia up 703% and Choice Hotels up 247% W/W. Giant movement off of a tiny base of spend, but it is encouraging to see.

TWO webinars to note:

THIS Friday June 5 at 11:30am EST, we will continue our analysis of relevant trends from Industry and Advertiser data. We will also hear insights from publishers, and what strategies they've been taking. You can register here.

Wednesday June 10 at 12pm, Andy Ellenthal will be joined by speakers from Duration Media, Pubmatic, and Confiant, to discuss actionable ideas that help to drive revenue for publishers. You can register here.

Below is a weekly view of the top 50 advertisers, based on spend. The right column compares last week to the average of the last 21 weeks.

The most noticeable trend this week is overall category movement instead of specific advertisers. Is this a result of “follow the leader”, or a semblance of normalcy returning to the market?

The Mobile & Wireless category having another big week. Up 48% led by AT&T, Verizon, and T-Mobile.

Software continues to show significant gains, dominated by another huge week for Adobe and their Creative Cloud, as well as Microsoft.

Pharma growing with Eli Lilly and Sanofi having their largest gains of the year. GSK who’s noticeably absent fell out of the Top 50 this week.

Insurance up. Driven by Liberty Mutual and State Farm. State Farm remains one of most consistent spenders.

Google has it’s strongest spending week of the year. Are they looking to make up gains from small businesses?

Other notable gainers: Clorox is back, indicating a return to store shelves. Home Depot and Lowe’s had big weeks, likely driven by the holiday weekend.

Keeping an eye on: When will these bellwether advertisers we believe are indicative of market health come back? Expedia, Pepsi, McDonalds, Fiat Chrysler, and Marriott. Are you seeing movement from any of these?

In case you missed Friday’s Webinar, there was extensive analysis of weekly advertiser data. Click here to see what was covered in the presentation.

A Note About The Data:

In an effort to make this advertising data more actionable, we've created a longer view to better spot trends by category and advertiser. The goal is to provide a picture that encompasses pre-Covid activity. The longer term view enables you to better capitalize on opportunities as advertiser spend returns.

Below is a weekly view of the top 50 advertisers, based on spend, over the last 20 weeks. The right column compares last week to the average of the last 20 weeks.

21 Advertisers are up Last Week vs. Average (20 weeks).

Notice AdWords is up and showing consistent growth in the past few weeks. We view AdWords as an indicator of auction pressure.

The Mobile & Wireless Category had a big week. AT&T is no longer social distancing.

This new view shows the extent of Auto’s drop, by far the biggest category for our BMX clients.

Adobe pops with their strongest week of the year with their push of the Creative Cloud. Fingers crossed advertisers will be ready with post-Covid creative.

Eli Lilly, Sanofi up. GSK not spending. What are the “right” drugs to get advertising support now?

Keeping an eye on: When QSR will pop. We are calling Dunkin as the leading indicator of the market return. Commuters, limited drive thru’s, no current spending. Which advertisers are you watching? (We aren’t holding our breath for travel)

New this week: Kick off your Memorial day weekend with some never before seen cuts of BMX data. Join our webinar on Friday at 1pm EST. If you haven’t already, register here.

Below are the top 50 advertisers, based on spend, on a week over week basis. The second column shows last week versus the prior 28 days.

Reminder: While W/W is an indicator of an advertiser's spending, a longer view provides a better measure of their actual spending trends.

27 Advertisers up W/W. Last week 19. 28 Advertisers are up over the last 28 days.

Adobe more than doubled spend over the last week. With marketing focused on their Creative Cloud, a new wave of ads may appear.

After a slow return, Insurance picking up with 5 advertisers gaining W/W, including Liberty Mutual, Berkshire Hathaway (largely driven by GEICO), and USAA

Disney, Microsoft, and Verizon maintain a steady climb upwards, unlike others in the top 50

Auto having another off week, with only Ford up W/W vs 5 advertisers up 2 weeks ago. FCA down big.

To note this week: Clorox makes an appearance in the top 50, a sign they may be back in the supply chain, or pushing other products?

Below are the top 50 advertisers, based on spend, on a week over week basis. The second column shows last week versus the prior 28 days.

Reminder: While W/W is an indicator of an advertiser's spending, a longer view provides a better measure of their actual spending trends.

19 Advertisers up W/W. Last week 24. 23 Advertisers are up over the last 28 days.

P&G picking up spend in the last 2 weeks a positive sign as the category leader attracts followers

Disney and eBay showing significant increases as consumer trends lean towards Entertainment, Online Shopping

Activision the largest gainer from last week, the largest decliner this week

After multiple weeks of increased spending, Auto was down with only Toyota up W/W

Other notable W/W gainers outside of the Top 50 are Apple, Kroger and L'Oreal, all leaders in their categories and great to see spending.

Below are the top 50 advertisers, based on spend, on a week over week basis. The second column shows last week versus the prior 28 days.

While W/W is an indicator of an advertiser's spending, a longer view provides a better measure of their actual spending trends.

30 Advertisers up W/W. Last week 24. While the last 2 weeks have been a low point, 27 Advertisers are up over the last 28 days.

5 Auto Advertisers are up (or flat) vs. 4 last week, with FCA being the biggest gainer again W/W

Wayfair and Johnson & Johnson up significantly, as Home Goods/ CPG return to the Top 15

Adwords up W/W, likely due to Small Business Credits from Google

Gaming and Computers up, with Activision being the highest gainer in the last week

Following drastic CPM drops in March and early April, we have seen less pronounced fluctuations throughout the month.

CPMs increased April 18-19 following weekend trends

A good sign: CPMs have increased 7% Monday (April 20) over prior Monday.

Facebook CPMs continue to impress following a drop at the end of March.

TripleLift CPMs have continued to increase since April 14.

AdX and AppNexus CPMs have remained stable, while most others experienced a decline in early April.

Games/Tech CPMs have been holding steady.

Both News and Lifestyle/Entertainment CPMs have been stable month-to-date.

Sports CPMs experienced an increase over the weekend of April 18-19 but have remained stable throughout April.

A Note About the Data: One day does not make a trend. We have learned that we need to see 3-5 days to see true movements on the data, like the April 11 CPM increase and Facebook's CPM drop on April 17.

Don’t Forget to register for our INSIGHTS by STAQ presentation next Friday, where we will further explore CPM trends along with additional relevant analysis across our dataset.

Click here to access your Benchmarking portal or contact your STAQ Account manager to find custom insights you can leverage

*The data in this email compares programmatic industry performance, running through STAQ systems for April 2020. This view excludes a publisher and a partner*

Below are the top 50 advertisers, based on spend, on a week over week basis. The second column shows last week versus the prior 28 days.

24 Advertisers up W/W. Last week 19.

4 Auto Advertisers are up, with FCA being the biggest gainer W/W

Citigroup up in a big way, Wells Fargo the other bank in the Top 50 down drastically. Discover out of Top 50 since last week.

Uber, down the last few weeks, is back up, likely due to Uber Eats

STAQ Benchmark Customer,

It has been a month (yes, only a month) since many of us realized the world was changing. I hope you and your family are staying safe, healthy, and sane.

From my perspective, everyone is approaching the sane part differently. STAQ’s CFO now runs 5 miles per day. My wife is doing online yoga. My personal goal, which I am crushing, is to stay hydrated.

My work goal is for our customers to receive as much value as possible from STAQ. You have been willing to contribute your data anonymously in our benchmark pool. In exchange we’ve made a commitment to offering insights and analysis in an effort to provide you, our valued partners, with as much actionable intelligence as possible.

To that end, we will begin sending the below report every Tuesday morning. We hope these views give you increased market insight and contain the early signs of when budgets return in earnest.

It highlights how the top 50 advertisers, based on spend, have changed on a week over week basis. The second column shows last week versus the prior 28 days.

Additionally, if any custom cuts of the benchmark data are valuable to you and your team, please reach out.

All my best,

Andy Ellenthal

CEO, STAQ

Looking at the first 21 days of March, we observed revenue drop by 6% and CPMs drop by 19%, while impressions increased by 16% YoY.

We typically see CPMs pop towards the end of Q1, but have observed 2020 CPMs consistently trending down since March 9th.

Good news is that CPMs appear to have plateaued following March 19th. We’re not sure how long this trend will continue, as we typically observe CPMs drop at the start of April.

After consistent CPM downturn, AdX CPMs along with Amazon, Rubicon, AppNexus, and Index Exchange have also flattened following March 19th. AdX’s plateau may be attributed to the rumors we’ve heard that Google is absorbing AdX fees to support publishers. Can anyone help validate?

Coming this Friday

We’ve previously only touched upon video specific trends. On Friday, we will be releasing a comprehensive dive into February and March video trends, available only to Benchmarking Clients.

*The data in this email compares programmatic industry performance, running through STAQ systems for March 2019, April 2019, and March 2020.*

Given the overwhelming response to last week’s newsletter on Coronavirus’ impact on ad spend, we’ve continued our industry analysis. Expanding on verticals, we’ve focused on select advertisers as well. Our findings compare the first week of March 2020 to that of February 2020.

Today’s data is through March 9th. As major announcements on March 11th (cancelling most sporting events, Travel Ban, etc) mark a turning point in the public response to the virus, we will be tracking further impact on the market. For those interested, we are offering a deeper dive via a webinar next Friday at 2pm EST. Please sign up via this link to reserve your spot. This is only available to BMX customers.

Finance decreased 36%, dropping from 15th to 24th.

Capital One decreased 30% and E-Trade decreased 32%. This may be attributed to recent market volatility.

Credit & Lending decreased 30%, falling from 10th to 14th.

Rock Holdings (Quicken Loans and Lower My Bills) decreased 23%.

Food & Grocery dropped from 27th to 32nd, decreasing 20%.

The Kroger Co. decreased 23%. We anticipate this vertical to increase in the next few weeks.

Consumer Goods grew 23% and is now 21st up from 26th.

The largest mover was Unilever which increased 335%. We expect this vertical to grow as well.

Interestingly, Travel increased 26%, growing from 14 to 11.

Expedia increased 24%. We suspect this vertical will decrease moving forward.

Government increased 169%, from 33rd to 10th.

U.S. Government was the biggest mover, growing 150%.

* The data in this email compares programmatic advertiser industry performance, running through STAQ systems for March 2019, February 2020, and March 2020.

The Coronavirus has made an impact on almost everything in our daily lives from the stock market to our advertiser benchmarks. We started to see revenue rise in health related industry verticals in February while travel related verticals have decreased.

Comparing top verticals from February 2020 to February 2019, we’ve observed:

Pharmaceuticals & Biotech revenue increased a staggering 175% YoY and is now the 2nd highest revenue vertical in 2020 up from 11th in 2019.

Pharmacy rose from 35th to 21st in 2020, increasing revenue 171%.

Travel revenue decreased 29%, falling from 17th to 33rd in 2020.

Other notable vertical movers:

Shopping decreased by 46%, falling from 23rd to 37th.

Consumer Electronics decreased by 52%, falling from 6th to 25th.

* The data in this email compares programmatic advertiser industry performance, running through STAQ systems for February 2019 and February 2020.

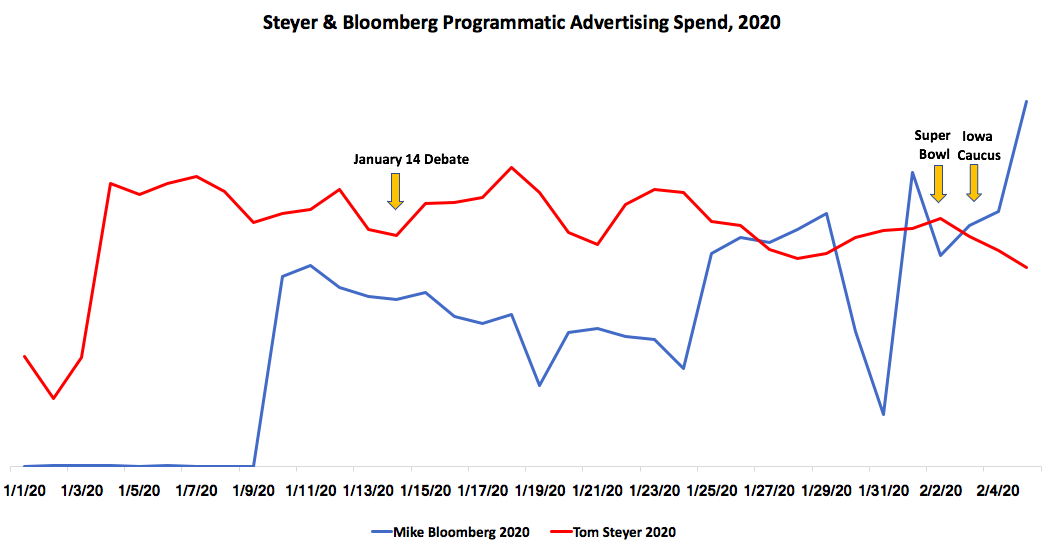

Note on the Data: This data compares programmatic advertising spend running through STAQ systems from September 2019 to February 2020 across 10+ partners. Of the advertisers in our Politics & Advocacy vertical, the analysis below is focused on the top 2 programmatic spenders: Tom Steyer and Mike Bloomberg.

We observed that 2-5 days leading up to a debate or the Iowa Caucus, Bloomberg picked up spend while Steyer remained consistent.

Leading up to the Iowa Caucus, on February 1, Bloomberg drastically increased spend overnight by almost 467%.

To put this in perspective: In 2020, across the publishers and partners where we’ve seen spend, candidates Steyer and Bloomberg are amongst the top 15 advertisers, and together have spent more than AT&T, Procter & Gamble, Apple, and Capital One combined.

From September 2019 to January 2020, we observed a sharp increase in spend in our Politics & Advocacy vertical as the election season heated up.

The largest MoM growth occurred from December 2019 to January 2020.

Steyer increased spend by 412% and Bloomberg by 782%.

Steyer, one of the highest spenders, comprised 59% of the Politics & Advocacy vertical spend.

Over 5 months, he outspent Microsoft and Progressive Insurance.

Since announcing his bid in late November, Bloomberg quickly became a top spender, accounting for 18% of spend in Politics & Advocacy.

Dates to Note:

Bloomberg announces bid for presidency - November 24

Debates - January 14, February 7, February 19, February 25

Iowa Caucus - February 3

Super Tuesday - March 3

Want to know which DSPs see the most political spend? How about which candidate is the most promiscuous in their DSP choices? Contact your STAQ Account Manager to find out!

Advertisers Move Spend To Android

Christmas In July For Desktop CPMs

CPMs Grow Despite Privacy Changes

Advertisers Want Guarantees Over Flexibility

Prepare For Advertisers To Re-Open Spend

Privacy Changes May Already Be Impacting Programmatic

Is Everyone Getting GM Spend Except You?

Advertisers Spending With Velocity

8 Prospects That Increased PG By 100%

Travel Advertiser’s Regaining Their Status

Taxes Are A Bright Spot For Publishers

Advertiser Momentum Picking Up

We Have A New View On Advertiser Spend

Good CPM News To Start The New Year

When The Ball Drops, Hopefully CPMs Don’t

Publishers Get Higher CPMs For The Holidays

Advertisers Come Home For The Holidays

Fashion Tip: Slippers Out, Sneakers In

CPM’s Soar As Advertisers Reset For Q4

Capabilities / Integrations / Careers / About / News / Contact / Privacy Policy

Copyright © 2021 STAQ. All Rights Reserved.